Examples

A number of examples of how to use Nempy are provided below. Examples 1 to 5 are simple and aim introduce various market features that can be modelled with Nempy in an easy to understand way, the dispatch and pricing outcomes are explained in inline comments where the results are printed. Examples 6 and 7 show how to use the historical data input preparation tools provided with Nempy to recreate historical dispatch intervals. Historical dispatch and pricing outcomes can be difficult to interpret as they are usually the result of complex interactions between the many features of the dispatch process, for these example the results are plotted in comparison to historical price outcomes. Example 8 demonstrates how the outputs of one dispatch interval can be used as the initial conditions of the next dispatch interval to create a time sequential model, additionally the current limitations with the approach are briefly discussed.

1. Bid stack equivalent market

This example implements a one region bid stack model of an electricity market. Under the bid stack model, generators are dispatched according to their bid prices, from cheapest to most expensive, until all demand is satisfied. No loss factors, ramping constraints or other factors are considered.

1import pandas as pd

2from nempy import markets

3

4# Volume of each bid, number of bands must equal number of bands in price_bids.

5volume_bids = pd.DataFrame({

6 'unit': ['A', 'B'],

7 '1': [20.0, 50.0], # MW

8 '2': [20.0, 30.0], # MW

9 '3': [5.0, 10.0] # More bid bands could be added.

10})

11

12# Price of each bid, bids must be monotonically increasing.

13price_bids = pd.DataFrame({

14 'unit': ['A', 'B'],

15 '1': [50.0, 50.0], # $/MW

16 '2': [60.0, 55.0], # $/MW

17 '3': [100.0, 80.0] # . . .

18})

19

20# Other unit properties

21unit_info = pd.DataFrame({

22 'unit': ['A', 'B'],

23 'region': ['NSW', 'NSW'], # MW

24})

25

26# The demand in the region\s being dispatched

27demand = pd.DataFrame({

28 'region': ['NSW'],

29 'demand': [115.0] # MW

30})

31

32# Create the market model

33market = markets.SpotMarket(unit_info=unit_info, market_regions=['NSW'])

34market.set_unit_volume_bids(volume_bids)

35market.set_unit_price_bids(price_bids)

36market.set_demand_constraints(demand)

37

38# Calculate dispatch and pricing

39market.dispatch()

40

41# Return the total dispatch of each unit in MW.

42print(market.get_unit_dispatch())

43# unit service dispatch

44# 0 A energy 35.0

45# 1 B energy 80.0

46

47# Understanding the dispatch results: Unit A's first bid is 20 MW at 50 $/MW,

48# and unit B's first bid is 50 MW at 50 $/MW, as demand for electricity is

49# 115 MW both these bids are need to meet demand and so both will be fully

50# dispatched. The next cheapest bid is 30 MW at 55 $/MW from unit B, combining

51# this with the first two bids we get 100 MW of generation, so all of this bid

52# will be dispatched. The next cheapest bid is 20 MW at 60 $/MW from unit A, by

53# dispatching 15 MW of this bid we get a total of 115 MW generation, and supply

54# meets demand so no more bids need to be dispatched. Adding up the dispatched

55# bids from each generator we can see that unit A will be dispatch for 35 MW

56# and unit B will be dispatch for 80 MW, as given by our bid stack market model.

57

58# Return the price of energy in each region.

59print(market.get_energy_prices())

60# region price

61# 0 NSW 60.0

62

63# Understanding the pricing result: In this case the marginal bid, the bid

64# that would be dispatch if demand increased is the 60 $/MW bid from unit

65# B, thus this bid sets the price.

66

67# Additional Detail: The above is a simplified interpretation

68# of the pricing result, note that the price is actually taken from the

69# underlying linear problem's shadow price for the supply equals demand constraint.

70# The way the problem is formulated if supply sits exactly between two bids,

71# for example at 120.0 MW, then the price is set by the lower rather

72# than the higher bid. Note, in practical use cases if the demand is a floating point

73# number this situation is unlikely to occur.

2. Unit loss factors, capacities and ramp rates

A simple example with two units in a one region market, units are given loss factors, capacity values and ramp rates. The effects of loss factors on dispatch and market prices are explained.

1import pandas as pd

2from nempy import markets

3

4# Volume of each bid, number of bands must equal number of bands in price_bids.

5volume_bids = pd.DataFrame({

6 'unit': ['A', 'B'],

7 '1': [20.0, 50.0], # MW

8 '2': [25.0, 30.0], # MW

9 '3': [5.0, 10.0] # More bid bands could be added.

10})

11

12# Price of each bid, bids must be monotonically increasing.

13price_bids = pd.DataFrame({

14 'unit': ['A', 'B'],

15 '1': [40.0, 50.0], # $/MW

16 '2': [60.0, 55.0], # $/MW

17 '3': [100.0, 80.0] # . . .

18})

19

20# Factors limiting unit output.

21unit_limits = pd.DataFrame({

22 'unit': ['A', 'B'],

23 'initial_output': [0.0, 0.0], # MW

24 'capacity': [55.0, 90.0], # MW

25 'ramp_up_rate': [600.0, 720.0], # MW/h

26 'ramp_down_rate': [600.0, 720.0] # MW/h

27})

28

29# Other unit properties including loss factors.

30unit_info = pd.DataFrame({

31 'unit': ['A', 'B'],

32 'region': ['NSW', 'NSW'], # MW

33 'loss_factor': [0.9, 0.95]

34})

35

36# The demand in the region\s being dispatched.

37demand = pd.DataFrame({

38 'region': ['NSW'],

39 'demand': [100.0] # MW

40})

41

42# Create the market model

43market = markets.SpotMarket(unit_info=unit_info,

44 market_regions=['NSW'])

45market.set_unit_volume_bids(volume_bids)

46market.set_unit_price_bids(price_bids)

47market.set_unit_bid_capacity_constraints(

48 unit_limits.loc[:, ['unit', 'capacity']])

49market.set_unit_ramp_rate_constraints(

50 unit_limits.loc[:, ['unit', 'initial_output', 'ramp_up_rate', 'ramp_down_rate']])

51market.set_demand_constraints(demand)

52

53# Calculate dispatch and pricing

54market.dispatch()

55

56# Return the total dispatch of each unit in MW.

57print(market.get_unit_dispatch())

58# unit service dispatch

59# 0 A energy 40.0

60# 1 B energy 60.0

61

62# Understanding the dispatch results: In this example unit loss factors are

63# provided, that means the cost of a bid in the dispatch optimisation is

64# the bid price divided by the unit loss factor. However, loss factors do

65# not effect the amount of generation a unit can supply, this is because the

66# regional demand already factors in intra regional losses. The cheapest bid is

67# from unit A with 20 MW at 44.44 $/MW (after loss factor), this will be

68# fully dispatched. The next cheapest bid is from unit B with 50 MW at

69# 52.63 $/MW, again fully dispatch. The next cheapest is unit B with 30 MW at

70# 57.89 $/MW, however, unit B starts the interval at a dispatch level of 0.0 MW

71# and can ramp at speed of 720 MW/hr, the default dispatch interval of Nempy

72# is 5 min, so unit B can at most produce 60 MW by the end of the

73# dispatch interval, this means only 10 MW of the second bid from unit B can be

74# dispatched. Finally, the last bid that needs to be dispatch for supply to

75# equal demand is from unit A with 25 MW at 66.67 $/MW, only 20 MW of this

76# bid is needed. Adding together the bids from each unit we can see that

77# unit A is dispatch for a total of 40 MW and unit B for a total of 60 MW.

78

79# Return the price of energy in each region.

80print(market.get_energy_prices())

81# region price

82# 0 NSW 66.67

83

84# Understanding the pricing result: In this case the marginal bid, the bid

85# that would be dispatch if demand increased is the second bid from unit A,

86# after adjusting for the loss factor this bid has a price of 66.67 $/MW bid,

87# and this bid sets the price.

3. Interconnector with losses

A simple example demonstrating how to implement a two region market with an interconnector. The interconnector is modelled simply, with a fixed percentage of losses. To make the interconnector flow and loss calculation easy to understand a single unit is modelled in the NSW region, NSW demand is set zero, and VIC region demand is set to 90 MW, thus all the power to meet VIC demand must flow across the interconnetcor.

1import pandas as pd

2from nempy import markets

3

4# The only generator is located in NSW.

5unit_info = pd.DataFrame({

6 'unit': ['A'],

7 'region': ['NSW'] # MW

8})

9

10# Create a market instance.

11market = markets.SpotMarket(unit_info=unit_info, market_regions=['NSW', 'VIC'])

12

13# Volume of each bids.

14volume_bids = pd.DataFrame({

15 'unit': ['A'],

16 '1': [100.0] # MW

17})

18

19market.set_unit_volume_bids(volume_bids)

20

21# Price of each bid.

22price_bids = pd.DataFrame({

23 'unit': ['A'],

24 '1': [50.0] # $/MW

25})

26

27market.set_unit_price_bids(price_bids)

28

29# NSW has no demand but VIC has 90 MW.

30demand = pd.DataFrame({

31 'region': ['NSW', 'VIC'],

32 'demand': [0.0, 90.0] # MW

33})

34

35market.set_demand_constraints(demand)

36

37# There is one interconnector between NSW and VIC. Its nominal direction is towards VIC.

38interconnectors = pd.DataFrame({

39 'interconnector': ['little_link'],

40 'to_region': ['VIC'],

41 'from_region': ['NSW'],

42 'max': [100.0],

43 'min': [-120.0]

44})

45

46market.set_interconnectors(interconnectors)

47

48

49# The interconnector loss function. In this case losses are always 5 % of line flow.

50def constant_losses(flow):

51 return abs(flow) * 0.05

52

53

54# The loss function on a per interconnector basis. Also details how the losses should be proportioned to the

55# connected regions.

56loss_functions = pd.DataFrame({

57 'interconnector': ['little_link'],

58 'from_region_loss_share': [0.5], # losses are shared equally.

59 'loss_function': [constant_losses]

60})

61

62# The points to linearly interpolate the loss function between. In this example the loss function is linear so only

63# three points are needed, but if a non linear loss function was used then more points would be better.

64interpolation_break_points = pd.DataFrame({

65 'interconnector': ['little_link', 'little_link', 'little_link'],

66 'loss_segment': [1, 2, 3],

67 'break_point': [-120.0, 0.0, 100]

68})

69

70market.set_interconnector_losses(loss_functions, interpolation_break_points)

71

72# Calculate dispatch.

73market.dispatch()

74

75# Return interconnector flow and losses.

76print(market.get_interconnector_flows())

77# interconnector flow losses

78# 0 little_link 92.307692 4.615385

79

80# Understanding the interconnector flows: Losses are modelled as extra demand

81# in the regions on either side of the interconnector, in this case the losses

82# are split evenly between the regions. All demand in VIC must be supplied

83# across the interconnector, and losses in VIC will add to the interconnector

84# flow required, so we can write the equation:

85#

86# flow = vic_demand + flow * loss_pct_vic

87# flow - flow * loss_pct_vic = vic_demand

88# flow * (1 - loss_pct_vic) = vic_demand

89# flow = vic_demand / (1 - loss_pct_vic)

90#

91# Since interconnector losses are 5% and half occur in VIC the

92# loss_pct_vic = 2.5%. Thus:

93#

94# flow = 90 / (1 - 0.025) = 92.31

95#

96# Knowing the interconnector flow we can work out total losses

97#

98# losses = flow * loss_pct

99# losses = 92.31 * 0.05 = 4.62

100

101# Return the total dispatch of each unit in MW.

102print(market.get_unit_dispatch())

103# unit service dispatch

104# 0 A energy 94.615385

105

106# Understanding dispatch results: Unit A must be dispatch to

107# meet supply in VIC plus all interconnector losses, therefore

108# dispatch is 90.0 + 4.62 = 94.62.

109

110# Return the price of energy in each region.

111print(market.get_energy_prices())

112# region price

113# 0 NSW 50.000000

114# 1 VIC 52.564103

115

116# Understanding pricing results: The marginal cost of supply in NSW is simply

117# the cost of unit A's bid. However, the marginal cost of supply in VIC also

118# includes the cost of paying for interconnector losses.

4. Dynamic non-linear interconnector losses

This example demonstrates how to model regional demand dependant interconnector loss functions as decribed in the AEMO

Marginal Loss Factors documentation section 3 to 5.

To make the interconnector flow and loss calculation easy to understand a single unit is modelled in the NSW region,

NSW demand is set zero, and VIC region demand is set to 800 MW, thus all the power to meet VIC demand must flow across

the interconnetcor.

1import pandas as pd

2from nempy import markets

3from nempy.historical_inputs import interconnectors as interconnector_inputs

4

5

6# The only generator is located in NSW.

7unit_info = pd.DataFrame({

8 'unit': ['A'],

9 'region': ['NSW'] # MW

10})

11

12# Create a market instance.

13market = markets.SpotMarket(unit_info=unit_info,

14 market_regions=['NSW', 'VIC'])

15

16# Volume of each bids.

17volume_bids = pd.DataFrame({

18 'unit': ['A'],

19 '1': [1000.0] # MW

20})

21

22market.set_unit_volume_bids(volume_bids)

23

24# Price of each bid.

25price_bids = pd.DataFrame({

26 'unit': ['A'],

27 '1': [50.0] # $/MW

28})

29

30market.set_unit_price_bids(price_bids)

31

32# NSW has no demand but VIC has 800 MW.

33demand = pd.DataFrame({

34 'region': ['NSW', 'VIC'],

35 'demand': [0.0, 800.0], # MW

36 'loss_function_demand': [0.0, 800.0] # MW

37})

38

39market.set_demand_constraints(demand.loc[:, ['region', 'demand']])

40

41# There is one interconnector between NSW and VIC.

42# Its nominal direction is towards VIC.

43interconnectors = pd.DataFrame({

44 'interconnector': ['VIC1-NSW1'],

45 'to_region': ['VIC'],

46 'from_region': ['NSW'],

47 'max': [1000.0],

48 'min': [-1200.0]

49})

50

51market.set_interconnectors(interconnectors)

52

53# Create a demand dependent loss function.

54# Specify the demand dependency

55demand_coefficients = pd.DataFrame({

56 'interconnector': ['VIC1-NSW1', 'VIC1-NSW1'],

57 'region': ['NSW1', 'VIC1'],

58 'demand_coefficient': [0.000021734, -0.000031523]})

59

60# Specify the loss function constant and flow coefficient.

61interconnector_coefficients = pd.DataFrame({

62 'interconnector': ['VIC1-NSW1'],

63 'loss_constant': [1.0657],

64 'flow_coefficient': [0.00017027],

65 'from_region_loss_share': [0.5]})

66

67# Create loss functions on per interconnector basis.

68loss_functions = interconnector_inputs.create_loss_functions(

69 interconnector_coefficients, demand_coefficients,

70 demand.loc[:, ['region', 'loss_function_demand']])

71

72# The points to linearly interpolate the loss function between.

73interpolation_break_points = pd.DataFrame({

74 'interconnector': 'VIC1-NSW1',

75 'loss_segment': [1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12],

76 'break_point': [-1200.0, -1000.0, -800.0, -600.0, -400.0, -200.0,

77 0.0, 200.0, 400.0, 600.0, 800.0, 1000]

78})

79

80market.set_interconnector_losses(loss_functions,

81 interpolation_break_points)

82

83# Calculate dispatch.

84market.dispatch()

85

86# Return interconnector flow and losses.

87print(market.get_interconnector_flows())

88# interconnector flow losses

89# 0 VIC1-NSW1 860.102737 120.205473

90

91# Understanding the interconnector flows: In this case it is not simple to

92# analytically derive and explain the interconnector flow result. The loss

93# model is constructed within the underlying mixed integer linear problem

94# as set of constraints and the interconnector flow and losses are

95# determined as part of the problem solution. However, the loss model can

96# be explained at a high level, and the results shown to be consistent. The

97# first step in the interconnector model is to drive the loss function as a

98# function of regional demand, which is a pre-market model creation step, the

99# mathematics is explained in

100# docs/pdfs/Marginal Loss Factors for the 2020-21 Financial year.pdf. The loss

101# function is then evaluated at the given break points and linearly interpolated

102# between those points in the market model. So for our model the losses are

103# interpolated between 800 MW and 1000 MW. We can show the losses are consistent

104# with this approach:

105#

106# Losses at a flow of 800 MW

107print(loss_functions['loss_function'].iloc[0](800))

108# 107.0464

109# Losses at a flow of 1000 MW

110print(loss_functions['loss_function'].iloc[0](1000))

111# 150.835

112# Then interpolating by taking the weighted sum of the two losses based on the

113# relative difference between the actual flow and the interpolation break points:

114# Weighting of 800 MW break point = 1 - ((860.102737 - 800.0)/(1000 - 800))

115# Weighting of 800 MW break point = 0.7

116# Weighting of 1000 MW break point = 1 - ((1000 - 860.102737)/(1000 - 800))

117# Weighting of 1000 MW break point = 0.3

118# Weighed sum of losses = 107.0464 * 0.7 + 150.835 * 0.3 = 120.18298

119#

120# We can also see that the flow and loss results are consistent with the supply

121# equals demand constraint, all demand in the VIC region is supplied by the

122# interconnector, so the interconnector flow minus the VIC region interconnector

123# losses should equal the VIC region demand. Note that the VIC region loss

124# share is 50%:

125# VIC region demand = interconnector flow - losses * VIC region loss share

126# 800 = 860.102737 - 120.205473 * 0.5

127# 800 = 800

128

129# Return the total dispatch of each unit in MW.

130print(market.get_unit_dispatch())

131# unit service dispatch

132# 0 A energy 920.205473

133

134# Understanding the dispatch results: Unit A is the only generator and it must

135# be dispatched to meet demand plus losses:

136# dispatch = VIC region demand + NSW region demand + losses

137# dispatch = 920.205473

138

139# Return the price of energy in each region.

140print(market.get_energy_prices())

141# region price

142# 0 NSW 50.000000

143# 1 VIC 62.292869

144

145# Understanding the pricing results: Pricing in the NSW region is simply the

146# marginal cost of supply from unit A. The marginal cost of supply in the

147# VIC region is the cost of unit A to meet both marginal demand and the

148# marginal losses on the interconnector.

5. Simple FCAS markets

This example implements a market for energy, regulation raise and contingency 6 sec raise, with

co-optimisation constraints as described in section 6.2 and 6.3 of

FCAS Model in NEMDE.

1import pandas as pd

2from nempy import markets

3

4

5# Set options so you see all DataFrame columns in print outs.

6pd.options.display.width = 0

7

8# Volume of each bid.

9volume_bids = pd.DataFrame({

10 'unit': ['A', 'A', 'B', 'B', 'B'],

11 'service': ['energy', 'raise_6s', 'energy',

12 'raise_6s', 'raise_reg'],

13 '1': [100.0, 10.0, 110.0, 15.0, 15.0], # MW

14})

15

16print(volume_bids)

17# unit service 1

18# 0 A energy 100.0

19# 1 A raise_6s 10.0

20# 2 B energy 110.0

21# 3 B raise_6s 15.0

22# 4 B raise_reg 15.0

23

24# Price of each bid.

25price_bids = pd.DataFrame({

26 'unit': ['A', 'A', 'B', 'B', 'B'],

27 'service': ['energy', 'raise_6s', 'energy',

28 'raise_6s', 'raise_reg'],

29 '1': [50.0, 35.0, 60.0, 20.0, 30.0], # $/MW

30})

31

32print(price_bids)

33# unit service 1

34# 0 A energy 50.0

35# 1 A raise_6s 35.0

36# 2 B energy 60.0

37# 3 B raise_6s 20.0

38# 4 B raise_reg 30.0

39

40# Participant defined operational constraints on FCAS enablement.

41fcas_trapeziums = pd.DataFrame({

42 'unit': ['B', 'B', 'A'],

43 'service': ['raise_reg', 'raise_6s', 'raise_6s'],

44 'max_availability': [15.0, 15.0, 10.0],

45 'enablement_min': [50.0, 50.0, 70.0],

46 'low_break_point': [65.0, 65.0, 80.0],

47 'high_break_point': [95.0, 95.0, 100.0],

48 'enablement_max': [110.0, 110.0, 110.0]

49})

50

51print(fcas_trapeziums)

52# unit service max_availability enablement_min low_break_point high_break_point enablement_max

53# 0 B raise_reg 15.0 50.0 65.0 95.0 110.0

54# 1 B raise_6s 15.0 50.0 65.0 95.0 110.0

55# 2 A raise_6s 10.0 70.0 80.0 100.0 110.0

56

57# Unit locations.

58unit_info = pd.DataFrame({

59 'unit': ['A', 'B'],

60 'region': ['NSW', 'NSW']

61})

62

63print(unit_info)

64# unit region

65# 0 A NSW

66# 1 B NSW

67

68# The demand in the region\s being dispatched.

69demand = pd.DataFrame({

70 'region': ['NSW'],

71 'demand': [195.0] # MW

72})

73

74print(demand)

75# region demand

76# 0 NSW 195.0

77

78# FCAS requirement in the region\s being dispatched.

79fcas_requirements = pd.DataFrame({

80 'set': ['nsw_regulation_requirement', 'nsw_raise_6s_requirement'],

81 'region': ['NSW', 'NSW'],

82 'service': ['raise_reg', 'raise_6s'],

83 'volume': [10.0, 10.0] # MW

84})

85

86print(fcas_requirements)

87# set region service volume

88# 0 nsw_regulation_requirement NSW raise_reg 10.0

89# 1 nsw_raise_6s_requirement NSW raise_6s 10.0

90

91# Create the market model with unit service bids.

92market = markets.SpotMarket(unit_info=unit_info,

93 market_regions=['NSW'])

94market.set_unit_volume_bids(volume_bids)

95market.set_unit_price_bids(price_bids)

96

97# Create constraints that enforce the top of the FCAS trapezium.

98fcas_availability = fcas_trapeziums.loc[:, ['unit', 'service', 'max_availability']]

99market.set_fcas_max_availability(fcas_availability)

100

101# Create constraints that enforce the lower and upper slope of the FCAS regulation

102# service trapeziums.

103regulation_trapeziums = fcas_trapeziums[fcas_trapeziums['service'] == 'raise_reg'].copy()

104market.set_energy_and_regulation_capacity_constraints(regulation_trapeziums)

105

106# Create constraints that enforce the lower and upper slope of the FCAS contingency

107# trapezium. These constraints also scale slopes of the trapezium to ensure the

108# co-dispatch of contingency and regulation services is technically feasible.

109contingency_trapeziums = fcas_trapeziums[fcas_trapeziums['service'] == 'raise_6s'].copy()

110market.set_joint_capacity_constraints(contingency_trapeziums)

111

112# Set the demand for energy.

113market.set_demand_constraints(demand)

114

115# Set the required volume of FCAS services.

116market.set_fcas_requirements_constraints(fcas_requirements)

117

118# Calculate dispatch and pricing

119market.dispatch()

120

121# Return the total dispatch of each unit in MW.

122print(market.get_unit_dispatch())

123# unit service dispatch

124# 0 A energy 100.0

125# 1 A raise_6s 5.0

126# 2 B energy 95.0

127# 3 B raise_6s 5.0

128# 4 B raise_reg 10.0

129

130# Understanding the dispatch results: Starting with the raise regulation

131# service we can see that only unit B has bid to provide this service so

132# 10 MW of its raise regulation bid must be dispatch. For the raise 6 s

133# service while unit B is cheaper it's provision of 10 MW of raise

134# regulation means it can only provide 5 MW of raise 6 s, so 5 MW must be

135# provided by unit A. For the energy service unit A is cheaper so all

136# 100 MW of its energy bid are dispatched, leaving the remaining 95 MW to

137# provided by unit B. Also, note that these energy and FCAS dispatch levels are

138# permitted by the FCAS trapezium constraints. Further explanation of these

139# constraints are provided here: docs/pdfs/FCAS Model in NEMDE.pdf.

140

141# Return the price of energy.

142print(market.get_energy_prices())

143# region price

144# 0 NSW 75.0

145

146# Understanding energy price results:

147# A marginal unit of energy would have to come from unit B, as unit A is fully

148# dispatch, this would cost 60 $/MW/h. However, to turn unit B up, you would

149# need it to dispatch less raise_6s, this would cost - 20 $/MW/h, and the

150# extra FCAS would have to come from unit A, this would cost 35 $/MW/h.

151# Therefore, the marginal cost of energy is 60 - 20 + 35 = 75 $/MW/h

152

153# Return the price of regulation FCAS.

154print(market.get_fcas_prices())

155# region service price

156# 0 NSW raise_6s 35.0

157# 1 NSW raise_reg 45.0

158

159# Understanding FCAS price results:

160# A marginal unit of raise_reg would have to come from unit B as it is the only

161# provider, this would cost 30 $/MW/h. It would also require unit B to provide

162# less raise_6s, this would cost -20 $/MW/h, extra raise_6s would then be

163# required from unit A costing 35 $/MW/h. This gives a total marginal cost of

164# 30 - 20 + 35 = 45 $/MW/h.

165#

166# A marginal unit of raise_6s would be provided by unit A at a cost of 35$/MW/h/.

6. Simple recreation of historical dispatch

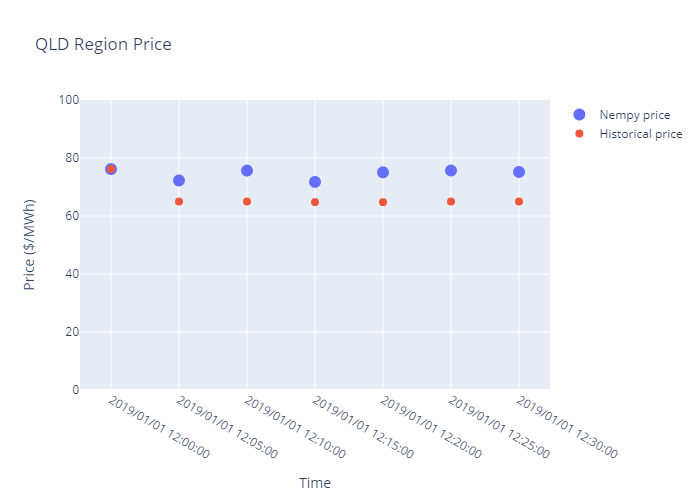

Demonstrates using Nempy to recreate historical dispatch intervals by implementing a simple energy market with unit bids, unit maximum capacity constraints and interconnector models, all sourced from historical data published by AEMO.

Results from example: for the QLD region a reasonable fit between modelled prices and historical prices is obtained.

Warning

Warning this script downloads approximately 8.5 GB of data from AEMO. The download_inputs flag can be set to false to stop the script re-downloading data for subsequent runs.

Note

This example also requires plotly >= 5.3.1, < 6.0.0 and kaleido == 0.2.1. Run pip install plotly==5.3.1 and pip install kaleido==0.2.1

1# Notice:

2# - This script downloads large volumes of historical market data from AEMO's nemweb

3# portal. The boolean on line 20 can be changed to prevent this happening repeatedly

4# once the data has been downloaded.

5# - This example also requires plotly >= 5.3.1, < 6.0.0 and kaleido == 0.2.1

6# pip install plotly==5.3.1 and pip install kaleido==0.2.1

7

8import sqlite3

9import pandas as pd

10import plotly.graph_objects as go

11from nempy import markets

12from nempy.historical_inputs import loaders, mms_db, \

13 xml_cache, units, demand, interconnectors

14

15con = sqlite3.connect('historical_mms.db')

16mms_db_manager = mms_db.DBManager(connection=con)

17

18xml_cache_manager = xml_cache.XMLCacheManager('nemde_cache')

19

20# The second time this example is run on a machine this flag can

21# be set to false to save downloading the data again.

22download_inputs = False

23

24if download_inputs:

25 # This requires approximately 5 GB of storage.

26 mms_db_manager.populate(start_year=2019, start_month=1,

27 end_year=2019, end_month=1)

28

29 # This requires approximately 3.5 GB of storage.

30 xml_cache_manager.populate_by_day(start_year=2019, start_month=1, start_day=1,

31 end_year=2019, end_month=1, end_day=1)

32

33raw_inputs_loader = loaders.RawInputsLoader(

34 nemde_xml_cache_manager=xml_cache_manager,

35 market_management_system_database=mms_db_manager)

36

37# A list of intervals we want to recreate historical dispatch for.

38dispatch_intervals = ['2019/01/01 12:00:00',

39 '2019/01/01 12:05:00',

40 '2019/01/01 12:10:00',

41 '2019/01/01 12:15:00',

42 '2019/01/01 12:20:00',

43 '2019/01/01 12:25:00',

44 '2019/01/01 12:30:00']

45

46# List for saving outputs to.

47outputs = []

48

49# Create and dispatch the spot market for each dispatch interval.

50for interval in dispatch_intervals:

51 raw_inputs_loader.set_interval(interval)

52 unit_inputs = units.UnitData(raw_inputs_loader)

53 demand_inputs = demand.DemandData(raw_inputs_loader)

54 interconnector_inputs = \

55 interconnectors.InterconnectorData(raw_inputs_loader)

56

57 unit_info = unit_inputs.get_unit_info()

58 market = markets.SpotMarket(market_regions=['QLD1', 'NSW1', 'VIC1',

59 'SA1', 'TAS1'],

60 unit_info=unit_info)

61

62 volume_bids, price_bids = unit_inputs.get_processed_bids()

63 market.set_unit_volume_bids(volume_bids)

64 market.set_unit_price_bids(price_bids)

65

66 unit_bid_limit = unit_inputs.get_unit_bid_availability()

67 market.set_unit_bid_capacity_constraints(unit_bid_limit)

68

69 unit_uigf_limit = unit_inputs.get_unit_uigf_limits()

70 market.set_unconstrained_intermittent_generation_forecast_constraint(

71 unit_uigf_limit)

72

73 regional_demand = demand_inputs.get_operational_demand()

74 market.set_demand_constraints(regional_demand)

75

76 interconnectors_definitions = \

77 interconnector_inputs.get_interconnector_definitions()

78 loss_functions, interpolation_break_points = \

79 interconnector_inputs.get_interconnector_loss_model()

80 market.set_interconnectors(interconnectors_definitions)

81 market.set_interconnector_losses(loss_functions,

82 interpolation_break_points)

83 market.dispatch()

84

85 # Save prices from this interval

86 prices = market.get_energy_prices()

87 prices['time'] = interval

88

89 # Getting historical prices for comparison. Note, ROP price, which is

90 # the regional reference node price before the application of any

91 # price scaling by AEMO, is used for comparison.

92 historical_prices = mms_db_manager.DISPATCHPRICE.get_data(interval)

93

94 prices = pd.merge(prices, historical_prices,

95 left_on=['time', 'region'],

96 right_on=['SETTLEMENTDATE', 'REGIONID'])

97

98 outputs.append(

99 prices.loc[:, ['time', 'region', 'price', 'ROP']])

100

101con.close()

102

103outputs = pd.concat(outputs)

104

105# Plot results for QLD market region.

106qld_prices = outputs[outputs['region'] == 'QLD1']

107

108fig = go.Figure()

109fig.add_trace(go.Scatter(x=qld_prices['time'], y=qld_prices['price'], name='Nempy price', mode='markers',

110 marker_size=12, marker_symbol='circle'))

111fig.add_trace(go.Scatter(x=qld_prices['time'], y=qld_prices['ROP'], name='Historical price', mode='markers',

112 marker_size=8))

113fig.update_xaxes(title="Time")

114fig.update_yaxes(title="Price ($/MWh)")

115fig.update_layout(yaxis_range=[0.0, 100.0], title="QLD Region Price")

116fig.write_image('energy_market_only_qld_prices.png')

117fig.show()

118

119print(outputs)

120# time region price ROP

121# 0 2019/01/01 12:00:00 NSW1 91.857666 91.87000

122# 1 2019/01/01 12:00:00 QLD1 76.180429 76.19066

123# 2 2019/01/01 12:00:00 SA1 85.126914 86.89938

124# 3 2019/01/01 12:00:00 TAS1 85.948523 89.70523

125# 4 2019/01/01 12:00:00 VIC1 83.250703 84.98410

126# 0 2019/01/01 12:05:00 NSW1 88.357224 91.87000

127# 1 2019/01/01 12:05:00 QLD1 72.255334 64.99000

128# 2 2019/01/01 12:05:00 SA1 82.417720 87.46213

129# 3 2019/01/01 12:05:00 TAS1 83.451561 90.08096

130# 4 2019/01/01 12:05:00 VIC1 80.621103 85.55555

131# 0 2019/01/01 12:10:00 NSW1 91.857666 91.87000

132# 1 2019/01/01 12:10:00 QLD1 75.665675 64.99000

133# 2 2019/01/01 12:10:00 SA1 85.680310 86.86809

134# 3 2019/01/01 12:10:00 TAS1 86.715499 89.87995

135# 4 2019/01/01 12:10:00 VIC1 83.774337 84.93569

136# 0 2019/01/01 12:15:00 NSW1 88.343034 91.87000

137# 1 2019/01/01 12:15:00 QLD1 71.746786 64.78003

138# 2 2019/01/01 12:15:00 SA1 82.379539 86.84407

139# 3 2019/01/01 12:15:00 TAS1 83.451561 89.48585

140# 4 2019/01/01 12:15:00 VIC1 80.621103 84.99034

141# 0 2019/01/01 12:20:00 NSW1 91.864122 91.87000

142# 1 2019/01/01 12:20:00 QLD1 75.052319 64.78003

143# 2 2019/01/01 12:20:00 SA1 85.722028 87.49564

144# 3 2019/01/01 12:20:00 TAS1 86.576848 90.28958

145# 4 2019/01/01 12:20:00 VIC1 83.859306 85.59438

146# 0 2019/01/01 12:25:00 NSW1 91.864122 91.87000

147# 1 2019/01/01 12:25:00 QLD1 75.696247 64.99000

148# 2 2019/01/01 12:25:00 SA1 85.746024 87.51983

149# 3 2019/01/01 12:25:00 TAS1 86.613642 90.38750

150# 4 2019/01/01 12:25:00 VIC1 83.894945 85.63046

151# 0 2019/01/01 12:30:00 NSW1 91.870167 91.87000

152# 1 2019/01/01 12:30:00 QLD1 75.188735 64.99000

153# 2 2019/01/01 12:30:00 SA1 85.694071 87.46153

154# 3 2019/01/01 12:30:00 TAS1 86.560602 90.09919

155# 4 2019/01/01 12:30:00 VIC1 83.843570 85.57286

7. Detailed recreation of historical dispatch with Basslink switch run

This example demonstrates using Nempy to recreate historical dispatch intervals by implementing an energy market using all the features of the Nempy market model, with inputs sourced from historical data published by AEMO. This example has been updated to include the use of functionality developed to enable modelling the Basslink switch run, which is new in Nempy version 2.0.0. Previously, Nempy relied on using the generic constraint RHS values reported with the NEMDE solution from what historically was the least cost case of the switch run. However, the new functionality allows the RHS values for each case of the switch run to be calculated by Nempy, and so for each case of switch run to be tested.

Warning

Warning this script downloads approximately 54 GB of data from AEMO. The download_inputs flag can be set to false to stop the script re-downloading data for subsequent runs.

1# Notice:

2# - This script downloads large volumes of historical market data (~54 GB) from AEMO's nemweb

3# portal. You can also reduce the data usage by restricting the time window given to the

4# xml_cache_manager and in the get_test_intervals function. The boolean on line 23 can

5# also be changed to prevent this happening repeatedly once the data has been downloaded.

6

7import sqlite3

8from datetime import datetime, timedelta

9import random

10import pandas as pd

11from nempy import markets

12from nempy.historical_inputs import loaders, mms_db, \

13 xml_cache, units, demand, interconnectors, constraints, rhs_calculator

14from nempy.help_functions.helper_functions import update_rhs_values

15

16con = sqlite3.connect('D:/nempy_2024_07/historical_mms.db')

17mms_db_manager = mms_db.DBManager(connection=con)

18

19xml_cache_manager = xml_cache.XMLCacheManager('D:/nempy_2024_07/xml_cache')

20

21# The second time this example is run on a machine this flag can

22# be set to false to save downloading the data again.

23download_inputs = True

24

25if download_inputs:

26 # This requires approximately 4 GB of storage.

27 mms_db_manager.populate(start_year=2024, start_month=7,

28 end_year=2024, end_month=7)

29

30 # This requires approximately 50 GB of storage.

31 xml_cache_manager.populate_by_day(start_year=2024, start_month=7, start_day=1,

32 end_year=2024, end_month=8, end_day=1)

33

34raw_inputs_loader = loaders.RawInputsLoader(

35 nemde_xml_cache_manager=xml_cache_manager,

36 market_management_system_database=mms_db_manager)

37

38

39# A list of intervals we want to recreate historical dispatch for.

40def get_test_intervals(number=100):

41 start_time = datetime(year=2024, month=7, day=1, hour=0, minute=0)

42 end_time = datetime(year=2024, month=8, day=1, hour=0, minute=0)

43 difference = end_time - start_time

44 difference_in_5_min_intervals = difference.days * 12 * 24

45 random.seed(1)

46 intervals = random.sample(range(1, difference_in_5_min_intervals), number)

47 times = [start_time + timedelta(minutes=5 * i) for i in intervals]

48 times_formatted = [t.isoformat().replace('T', ' ').replace('-', '/') for t in times]

49 return times_formatted

50

51

52# List for saving outputs to.

53outputs = []

54c = 0

55# Create and dispatch the spot market for each dispatch interval.

56for interval in get_test_intervals(number=100):

57 c += 1

58 print(str(c) + ' ' + str(interval))

59 raw_inputs_loader.set_interval(interval)

60 unit_inputs = units.UnitData(raw_inputs_loader)

61 interconnector_inputs = interconnectors.InterconnectorData(raw_inputs_loader)

62 constraint_inputs = constraints.ConstraintData(raw_inputs_loader)

63 demand_inputs = demand.DemandData(raw_inputs_loader)

64 rhs_calculation_engine = rhs_calculator.RHSCalc(xml_cache_manager)

65

66 unit_info = unit_inputs.get_unit_info()

67 market = markets.SpotMarket(market_regions=['QLD1', 'NSW1', 'VIC1',

68 'SA1', 'TAS1'],

69 unit_info=unit_info)

70

71 # Set bids

72 volume_bids, price_bids = unit_inputs.get_processed_bids()

73 market.set_unit_volume_bids(volume_bids)

74 market.set_unit_price_bids(price_bids)

75

76 # Set bid in capacity limits

77 unit_bid_limit = unit_inputs.get_unit_bid_availability()

78 market.set_unit_bid_capacity_constraints(unit_bid_limit)

79 cost = constraint_inputs.get_constraint_violation_prices()['unit_capacity']

80 market.make_constraints_elastic('unit_bid_capacity', violation_cost=cost)

81

82 # Set limits provided by the unconstrained intermittent generation

83 # forecasts. Primarily for wind and solar.

84 unit_uigf_limit = unit_inputs.get_unit_uigf_limits()

85 market.set_unconstrained_intermittent_generation_forecast_constraint(

86 unit_uigf_limit)

87 cost = constraint_inputs.get_constraint_violation_prices()['uigf']

88 market.make_constraints_elastic('uigf_capacity', violation_cost=cost)

89

90 ramp_rates = unit_inputs.get_bid_ramp_rates()

91 scada_ramp_rates = unit_inputs.get_scada_ramp_rates(inlude_initial_output=True)

92 initial_fast_start_profiles = unit_inputs.get_fast_start_profiles_for_dispatch()

93

94 # Set unit ramp rates.

95 def set_ramp_rates(run_type, fsp):

96 if run_type == "fast_start_first_run":

97 fsp = fsp.loc[:, ['unit', 'current_mode']]

98 else:

99 fsp = fsp.loc[:, ['unit', 'end_mode', 'time_since_end_of_mode_two', 'min_loading']]

100 cost = constraint_inputs.get_constraint_violation_prices()['ramp_rate']

101 market.set_unit_ramp_rate_constraints(

102 ramp_rates,

103 scada_ramp_rates.loc[:, ['unit', 'scada_ramp_up_rate', 'scada_ramp_down_rate']],

104 fsp,

105 run_type=run_type, violation_cost=cost

106 )

107 cost = constraint_inputs.get_constraint_violation_prices()['fcas_profile']

108 market.set_joint_ramping_constraints_reg(

109 scada_ramp_rates, fsp, run_type=run_type, violation_cost=cost

110 )

111

112

113 set_ramp_rates('fast_start_first_run', initial_fast_start_profiles)

114

115 # Set unit FCAS trapezium constraints.

116 unit_inputs.add_fcas_trapezium_constraints()

117 cost = constraint_inputs.get_constraint_violation_prices()['fcas_max_avail']

118 fcas_availability = unit_inputs.get_fcas_max_availability()

119 market.set_fcas_max_availability(fcas_availability, violation_cost=cost)

120 cost = constraint_inputs.get_constraint_violation_prices()['fcas_profile']

121 regulation_trapeziums = unit_inputs.get_fcas_regulation_trapeziums()

122 market.set_energy_and_regulation_capacity_constraints(regulation_trapeziums, violation_cost=cost)

123 contingency_trapeziums = unit_inputs.get_contingency_services()

124 market.set_joint_capacity_constraints(contingency_trapeziums, violation_cost=cost)

125

126 # Set interconnector definitions, limits and loss models.

127 interconnectors_definitions = \

128 interconnector_inputs.get_interconnector_definitions()

129 loss_functions, interpolation_break_points = \

130 interconnector_inputs.get_interconnector_loss_model()

131 market.set_interconnectors(interconnectors_definitions)

132 market.set_interconnector_losses(loss_functions,

133 interpolation_break_points)

134

135 # Calculate rhs constraint values that depend on the basslink frequency controller from scratch so there is

136 # consistency between the basslink switch runs.

137 # Find the constraints that need to be calculated because they depend on the frequency controller status.

138 constraints_to_update = (

139 rhs_calculation_engine.get_rhs_constraint_equations_that_depend_value('BL_FREQ_ONSTATUS', 'W'))

140 initial_bl_freq_onstatus = rhs_calculation_engine.scada_data['W']['BL_FREQ_ONSTATUS'][0]['@Value']

141 # Calculate new rhs values for the constraints that need updating.

142 new_rhs_values = rhs_calculation_engine.compute_constraint_rhs(constraints_to_update)

143

144 # Add generic constraints and FCAS market constraints.

145 fcas_requirements = constraint_inputs.get_fcas_requirements()

146 fcas_requirements = update_rhs_values(fcas_requirements, new_rhs_values)

147 cost = constraint_inputs.get_violation_costs()

148 market.set_fcas_requirements_constraints(fcas_requirements, violation_cost=cost)

149 generic_rhs = constraint_inputs.get_rhs_and_type_excluding_regional_fcas_constraints()

150 generic_rhs = update_rhs_values(generic_rhs, new_rhs_values)

151 market.set_generic_constraints(generic_rhs, violation_cost=cost)

152

153 unit_generic_lhs = constraint_inputs.get_unit_lhs()

154 market.link_units_to_generic_constraints(unit_generic_lhs)

155 interconnector_generic_lhs = constraint_inputs.get_interconnector_lhs()

156 market.link_interconnectors_to_generic_constraints(

157 interconnector_generic_lhs)

158

159 # Set the operational demand to be met by dispatch.

160 regional_demand = demand_inputs.get_operational_demand()

161 cost = constraint_inputs.get_constraint_violation_prices()['regional_demand']

162 market.set_demand_constraints(regional_demand, violation_cost=cost)

163

164 # Set tiebreak constraint to equalise dispatch of equally priced bids.

165 cost = constraint_inputs.get_constraint_violation_prices()['tiebreak']

166 market.set_tie_break_constraints(cost)

167

168 # Get unit dispatch without fast start constraints and use it to

169 # make fast start unit commitment decisions.

170 market.dispatch()

171 dispatch = market.get_unit_dispatch()

172 fast_start_profiles = unit_inputs.get_fast_start_profiles_for_dispatch(dispatch)

173 set_ramp_rates('fast_start_second_run', fast_start_profiles)

174 cost = constraint_inputs.get_constraint_violation_prices()['fast_start']

175 cols = ['unit', 'end_mode', 'time_in_end_mode', 'mode_two_length',

176 'mode_four_length', 'min_loading']

177 fsp = fast_start_profiles.loc[:, cols]

178 market.set_fast_start_constraints(fsp, violation_cost=cost)

179

180 # First run of Basslink switch runs

181 market.dispatch() # First dispatch without allowing over constrained dispatch re-run to get objective function.

182 objective_value_run_one = market.objective_value

183 if constraint_inputs.is_over_constrained_dispatch_rerun():

184 market.dispatch(allow_over_constrained_dispatch_re_run=True,

185 energy_market_floor_price=-1000.0,

186 energy_market_ceiling_price=17500.0,

187 fcas_market_ceiling_price=1000.0)

188 prices_run_one = market.get_energy_prices() # If this is the lowest cost run these will be the market prices.

189

190 # Re-run dispatch with Basslink Frequency controller off.

191 # Set frequency controller to off in rhs calculations

192 rhs_calculation_engine.update_spd_id_value('BL_FREQ_ONSTATUS', 'W', '0')

193 new_bl_freq_onstatus = rhs_calculation_engine.scada_data['W']['BL_FREQ_ONSTATUS'][0]['@Value']

194 # Find the constraints that need to be updated because they depend on the frequency controller status.

195 constraints_to_update = (

196 rhs_calculation_engine.get_rhs_constraint_equations_that_depend_value('BL_FREQ_ONSTATUS', 'W'))

197 # Calculate new rhs values for the constraints that need updating.

198 new_rhs_values = rhs_calculation_engine.compute_constraint_rhs(constraints_to_update)

199 # Update the constraints in the market.

200 fcas_requirements = update_rhs_values(fcas_requirements, new_rhs_values)

201 cost = constraint_inputs.get_violation_costs()

202 market.set_fcas_requirements_constraints(fcas_requirements, violation_cost=cost)

203 generic_rhs = update_rhs_values(generic_rhs, new_rhs_values)

204 market.set_generic_constraints(generic_rhs, violation_cost=cost)

205

206 # Reset ramp rate constraints for first run of second Basslink switchrun

207 set_ramp_rates('fast_start_first_run', initial_fast_start_profiles)

208

209 # Get unit dispatch without fast start constraints and use it to

210 # make fast start unit commitment decisions.

211 market.remove_fast_start_constraints()

212 market.dispatch()

213 dispatch = market.get_unit_dispatch()

214 fast_start_profiles = unit_inputs.get_fast_start_profiles_for_dispatch(dispatch)

215 set_ramp_rates('fast_start_second_run', fast_start_profiles)

216 cost = constraint_inputs.get_constraint_violation_prices()['fast_start']

217 cols = ['unit', 'end_mode', 'time_in_end_mode', 'mode_two_length',

218 'mode_four_length', 'min_loading']

219 fsp = fast_start_profiles.loc[:, cols]

220 market.set_fast_start_constraints(fsp, violation_cost=cost)

221

222 market.dispatch() # First dispatch without allowing over constrained dispatch re-run to get objective function.

223 objective_value_run_two = market.objective_value

224 if constraint_inputs.is_over_constrained_dispatch_rerun():

225 market.dispatch(allow_over_constrained_dispatch_re_run=True,

226 energy_market_floor_price=-1000.0,

227 energy_market_ceiling_price=17500.0,

228 fcas_market_ceiling_price=1000.0)

229 prices_run_two = market.get_energy_prices() # If this is the lowest cost run these will be the market prices.

230

231 prices_run_one['time'] = interval

232 prices_run_two['time'] = interval

233

234 # Getting historical prices for comparison. Note, ROP price, which is

235 # the regional reference node price before the application of any

236 # price scaling by AEMO, is used for comparison.

237 historical_prices = mms_db_manager.DISPATCHPRICE.get_data(interval)

238

239 # The prices from the run with the lowest objective function value are used.

240 if objective_value_run_one < objective_value_run_two:

241 prices = prices_run_one

242 else:

243 prices = prices_run_two

244

245 prices['time'] = interval

246 prices = pd.merge(prices, historical_prices,

247 left_on=['time', 'region'],

248 right_on=['SETTLEMENTDATE', 'REGIONID'])

249

250 outputs.append(prices)

251

252con.close()

253

254outputs = pd.concat(outputs)

255

256outputs['error'] = outputs['price'] - outputs['ROP']

257

258print('\n Summary of error in energy price volume weighted average price. \n'

259 'Comparison is against ROP, the price prior to \n'

260 'any post dispatch adjustments, scaling, capping etc.')

261print('Mean price error: {}'.format(outputs['error'].mean()))

262print('Median price error: {}'.format(outputs['error'].quantile(0.5)))

263print('5% percentile price error: {}'.format(outputs['error'].quantile(0.05)))

264print('95% percentile price error: {}'.format(outputs['error'].quantile(0.95)))

265

266# Summary of error in energy price volume weighted average price.

267# Comparison is against ROP, the price prior to

268# any post dispatch adjustments, scaling, capping etc.

269# Mean price error: 0.15175124971435794

270# Median price error: 0.0

271# 5% percentile price error: -0.2187800690807549

272# 95% percentile price error: 0.027599033294391225

273

7. Recreation of historical dispatch without Basslink switchrun

This example demonstrates using Nempy to recreate historical dispatch intervals by implementing an energy market using all the features of the Nempy market model, except the Basslink switch run, with inputs sourced from historical data published by AEMO. The main reason not to include Basslink switch run is to speed up runtime. Note each interval is dispatched as a standalone simulation and the results from one dispatch interval are not carried over to be the initial conditions of the next interval, rather the historical initial conditions are always used.

Warning

Warning this script downloads approximately 54 GB of data from AEMO. The download_inputs flag can be set to false to stop the script re-downloading data for subsequent runs.

1# Notice:

2# - This script downloads large volumes of historical market data (~54 GB) from AEMO's nemweb

3# portal. You can also reduce the data usage by restricting the time window given to the

4# xml_cache_manager and in the get_test_intervals function. The boolean on line 22 can

5# also be changed to prevent this happening repeatedly once the data has been downloaded.

6

7import sqlite3

8from datetime import datetime, timedelta

9import random

10import pandas as pd

11from nempy import markets

12from nempy.historical_inputs import loaders, mms_db, \

13 xml_cache, units, demand, interconnectors, constraints

14

15con = sqlite3.connect('D:/nempy_2024_07/historical_mms.db')

16mms_db_manager = mms_db.DBManager(connection=con)

17

18xml_cache_manager = xml_cache.XMLCacheManager('D:/nempy_2024_07/xml_cache')

19

20# The second time this example is run on a machine this flag can

21# be set to false to save downloading the data again.

22download_inputs = True

23

24if download_inputs:

25 # This requires approximately 4 GB of storage.

26 mms_db_manager.populate(start_year=2024, start_month=7,

27 end_year=2024, end_month=7)

28

29 # This requires approximately 50 GB of storage.

30 xml_cache_manager.populate_by_day(start_year=2024, start_month=7, start_day=1,

31 end_year=2024, end_month=8, end_day=1)

32

33raw_inputs_loader = loaders.RawInputsLoader(

34 nemde_xml_cache_manager=xml_cache_manager,

35 market_management_system_database=mms_db_manager)

36

37

38# A list of intervals we want to recreate historical dispatch for.

39def get_test_intervals(number=100):

40 start_time = datetime(year=2024, month=7, day=1, hour=0, minute=0)

41 end_time = datetime(year=2024, month=8, day=1, hour=0, minute=0)

42 difference = end_time - start_time

43 difference_in_5_min_intervals = difference.days * 12 * 24

44 random.seed(1)

45 intervals = random.sample(range(1, difference_in_5_min_intervals), number)

46 times = [start_time + timedelta(minutes=5 * i) for i in intervals]

47 times_formatted = [t.isoformat().replace('T', ' ').replace('-', '/') for t in times]

48 return times_formatted

49

50

51# List for saving outputs to.

52outputs = []

53c = 0

54# Create and dispatch the spot market for each dispatch interval.

55for interval in get_test_intervals(number=100):

56

57 c += 1

58 print(str(c) + ' ' + str(interval))

59 raw_inputs_loader.set_interval(interval)

60 unit_inputs = units.UnitData(raw_inputs_loader)

61 interconnector_inputs = interconnectors.InterconnectorData(raw_inputs_loader)

62 constraint_inputs = constraints.ConstraintData(raw_inputs_loader)

63 demand_inputs = demand.DemandData(raw_inputs_loader)

64

65 unit_info = unit_inputs.get_unit_info()

66 market = markets.SpotMarket(market_regions=['QLD1', 'NSW1', 'VIC1',

67 'SA1', 'TAS1'],

68 unit_info=unit_info)

69

70 # Set bids

71 volume_bids, price_bids = unit_inputs.get_processed_bids()

72 market.set_unit_volume_bids(volume_bids)

73 market.set_unit_price_bids(price_bids)

74

75 # Set bid in capacity limits

76 unit_bid_limit = unit_inputs.get_unit_bid_availability()

77 cost = constraint_inputs.get_constraint_violation_prices()['unit_capacity']

78 market.set_unit_bid_capacity_constraints(unit_bid_limit, violation_cost=cost)

79

80 # Set limits provided by the unconstrained intermittent generation

81 # forecasts. Primarily for wind and solar.

82 unit_uigf_limit = unit_inputs.get_unit_uigf_limits()

83 cost = constraint_inputs.get_constraint_violation_prices()['uigf']

84 market.set_unconstrained_intermittent_generation_forecast_constraint(

85 unit_uigf_limit, violation_cost=cost

86 )

87

88 # Set unit ramp rates.

89 ramp_rates = unit_inputs.get_bid_ramp_rates()

90 scada_ramp_rates = unit_inputs.get_scada_ramp_rates()

91 fast_start_profiles = unit_inputs.get_fast_start_profiles_for_dispatch()

92 cost = constraint_inputs.get_constraint_violation_prices()['ramp_rate']

93 market.set_unit_ramp_rate_constraints(

94 ramp_rates, scada_ramp_rates, fast_start_profiles,

95 run_type="fast_start_first_run", violation_cost=cost

96 )

97

98 # Set unit FCAS trapezium constraints.

99 unit_inputs.add_fcas_trapezium_constraints()

100 cost = constraint_inputs.get_constraint_violation_prices()['fcas_max_avail']

101 fcas_availability = unit_inputs.get_fcas_max_availability()

102 market.set_fcas_max_availability(fcas_availability, violation_cost=cost)

103 cost = constraint_inputs.get_constraint_violation_prices()['fcas_profile']

104 regulation_trapeziums = unit_inputs.get_fcas_regulation_trapeziums()

105 market.set_energy_and_regulation_capacity_constraints(regulation_trapeziums,

106 violation_cost=cost)

107 scada_ramp_rates = unit_inputs.get_scada_ramp_rates(inlude_initial_output=True)

108 market.set_joint_ramping_constraints_reg(

109 scada_ramp_rates, fast_start_profiles, run_type="fast_start_first_run",

110 violation_cost=cost

111 )

112 contingency_trapeziums = unit_inputs.get_contingency_services()

113 market.set_joint_capacity_constraints(contingency_trapeziums, violation_cost=cost)

114

115 # Set interconnector definitions, limits and loss models.

116 interconnectors_definitions = \

117 interconnector_inputs.get_interconnector_definitions()

118 loss_functions, interpolation_break_points = \

119 interconnector_inputs.get_interconnector_loss_model()

120 market.set_interconnectors(interconnectors_definitions)

121 market.set_interconnector_losses(loss_functions,

122 interpolation_break_points)

123

124 # Add generic constraints and FCAS market constraints.

125 fcas_requirements = constraint_inputs.get_fcas_requirements()

126 cost = constraint_inputs.get_violation_costs()

127 market.set_fcas_requirements_constraints(fcas_requirements, violation_cost=cost)

128 generic_rhs = constraint_inputs.get_rhs_and_type_excluding_regional_fcas_constraints()

129 market.set_generic_constraints(generic_rhs, violation_cost=cost)

130 unit_generic_lhs = constraint_inputs.get_unit_lhs()

131 market.link_units_to_generic_constraints(unit_generic_lhs)

132 interconnector_generic_lhs = constraint_inputs.get_interconnector_lhs()

133 market.link_interconnectors_to_generic_constraints(interconnector_generic_lhs)

134

135 # Set the operational demand to be met by dispatch.

136 regional_demand = demand_inputs.get_operational_demand()

137 cost = constraint_inputs.get_constraint_violation_prices()['regional_demand']

138 market.set_demand_constraints(regional_demand, violation_cost=cost)

139

140 # Set tiebreak constraint to equalise dispatch of equally priced bids.

141 cost = constraint_inputs.get_constraint_violation_prices()['tiebreak']

142 market.set_tie_break_constraints(cost)

143

144 # Get unit dispatch without fast start constraints and use it to

145 # make fast start unit commitment decisions.

146 market.dispatch()

147 dispatch = market.get_unit_dispatch()

148

149 cost = constraint_inputs.get_constraint_violation_prices()['fast_start']

150 fast_start_profiles = unit_inputs.get_fast_start_profiles_for_dispatch(dispatch)

151 cols = ['unit', 'end_mode', 'time_in_end_mode', 'mode_two_length',

152 'mode_four_length', 'min_loading']

153 fsp = fast_start_profiles.loc[:, cols]

154 market.set_fast_start_constraints(fsp, violation_cost=cost)

155

156 ramp_rates = unit_inputs.get_bid_ramp_rates()

157 scada_ramp_rates = unit_inputs.get_scada_ramp_rates()

158 cols = ['unit', 'end_mode', 'time_since_end_of_mode_two', 'min_loading']

159 fsp = fast_start_profiles.loc[:, cols]

160 cost = constraint_inputs.get_constraint_violation_prices()['ramp_rate']

161 market.set_unit_ramp_rate_constraints(

162 ramp_rates, scada_ramp_rates, fsp,

163 run_type="fast_start_second_run", violation_cost=cost

164 )

165 cost = constraint_inputs.get_constraint_violation_prices()['fcas_profile']

166 scada_ramp_rates = unit_inputs.get_scada_ramp_rates(inlude_initial_output=True)

167 market.set_joint_ramping_constraints_reg(

168 scada_ramp_rates, fsp, run_type="fast_start_second_run", violation_cost=cost

169 )

170

171 # If AEMO historically used the over constrained dispatch rerun

172 # process then allow it to be used in dispatch. This is needed

173 # because sometimes the conditions for over constrained dispatch

174 # are present but the rerun process isn't used.

175 if constraint_inputs.is_over_constrained_dispatch_rerun():

176 market.dispatch(allow_over_constrained_dispatch_re_run=True,

177 energy_market_floor_price=-1000.0,

178 energy_market_ceiling_price=17500.0,

179 fcas_market_ceiling_price=1000.0)

180 else:

181 # The market price ceiling and floor are not needed here

182 # because they are only used for the over constrained

183 # dispatch rerun process.

184 market.dispatch(allow_over_constrained_dispatch_re_run=False)

185

186 # Save prices from this interval

187 prices = market.get_energy_prices()

188 prices['time'] = interval

189

190 # Getting historical prices for comparison. Note, ROP price, which is

191 # the regional reference node price before the application of any

192 # price scaling by AEMO, is used for comparison.

193 historical_prices = mms_db_manager.DISPATCHPRICE.get_data(interval)

194

195 prices = pd.merge(prices, historical_prices,

196 left_on=['time', 'region'],

197 right_on=['SETTLEMENTDATE', 'REGIONID'])

198

199 outputs.append(

200 prices.loc[:, ['time', 'region', 'price', 'ROP']])

201

202con.close()

203

204outputs = pd.concat(outputs)

205

206outputs['error'] = outputs['price'] - outputs['ROP']

207

208outputs.to_csv("bdu_prices.csv")

209

210print('\n Summary of error in energy price volume weighted average price. \n'

211 'Comparison is against ROP, the price prior to \n'

212 'any post dispatch adjustments, scaling, capping etc.')

213print('Mean price error: {}'.format(outputs['error'].mean()))

214print('Median price error: {}'.format(outputs['error'].quantile(0.5)))

215print('5% percentile price error: {}'.format(outputs['error'].quantile(0.05)))

216print('95% percentile price error: {}'.format(outputs['error'].quantile(0.95)))

217

218# Summary of error in energy price volume weighted average price.

219# Comparison is against ROP, the price prior to

220# any post dispatch adjustments, scaling, capping etc.

221# Mean price error: 0.13818277307210394

222# Median price error: 0.0

223# 5% percentile price error: -0.13335830516772942

224# 95% percentile price error: 0.013533539900288811

8. Time sequential recreation of historical dispatch

This example demonstrates using Nempy to recreate historical dispatch in a dynamic or time sequential manner, this means the outputs of one interval become the initial conditions for the next dispatch interval. Note, currently there is not the infrastructure in place to include features such as generic constraints in the time sequential model as the rhs values of many constraints would need to be re-calculated based on the dynamic system state. Similarly, using historical bids in this example is some what problematic as participants also dynamically change their bids based on market conditions. However, for the sake of demonstrating how Nempy can be used to create time sequential models, historical bids are used in this example.

Warning

Warning this script downloads approximately 8.5 GB of data from AEMO. The download_inputs flag can be set to false to stop the script re-downloading data for subsequent runs.

1# Notice:

2# - This script downloads large volumes of historical market data from AEMO's nemweb

3# portal. The boolean on line 20 can be changed to prevent this happening repeatedly

4# once the data has been downloaded.

5# - This example also requires plotly >= 5.3.1, < 6.0.0 and kaleido == 0.2.1

6# pip install plotly==5.3.1 and pip install kaleido==0.2.1

7

8import sqlite3

9import pandas as pd

10from nempy import markets, time_sequential

11from nempy.historical_inputs import loaders, mms_db, \

12 xml_cache, units, demand, interconnectors, constraints

13

14con = sqlite3.connect('market_management_system.db')

15mms_db_manager = mms_db.DBManager(connection=con)

16

17xml_cache_manager = xml_cache.XMLCacheManager('cache_directory')

18

19# The second time this example is run on a machine this flag can

20# be set to false to save downloading the data again.

21download_inputs = True

22

23if download_inputs:

24 # This requires approximately 5 GB of storage.

25 mms_db_manager.populate(start_year=2019, start_month=1,

26 end_year=2019, end_month=1)

27

28 # This requires approximately 3.5 GB of storage.

29 xml_cache_manager.populate_by_day(start_year=2019, start_month=1, start_day=1,

30 end_year=2019, end_month=1, end_day=1)

31

32raw_inputs_loader = loaders.RawInputsLoader(

33 nemde_xml_cache_manager=xml_cache_manager,

34 market_management_system_database=mms_db_manager)

35

36# A list of intervals we want to recreate historical dispatch for.

37dispatch_intervals = ['2019/01/01 12:00:00',

38 '2019/01/01 12:05:00',

39 '2019/01/01 12:10:00',

40 '2019/01/01 12:15:00',

41 '2019/01/01 12:20:00',

42 '2019/01/01 12:25:00',

43 '2019/01/01 12:30:00']

44

45# List for saving outputs to.

46outputs = []

47

48unit_dispatch = None

49from time import time

50

51t0 = time()

52# Create and dispatch the spot market for each dispatch interval.

53for interval in dispatch_intervals:

54 print(interval)

55 raw_inputs_loader.set_interval(interval)

56 unit_inputs = units.UnitData(raw_inputs_loader)

57 demand_inputs = demand.DemandData(raw_inputs_loader)

58 interconnector_inputs = \

59 interconnectors.InterconnectorData(raw_inputs_loader)

60 constraint_inputs = \

61 constraints.ConstraintData(raw_inputs_loader)

62

63 unit_info = unit_inputs.get_unit_info()

64 market = markets.SpotMarket(market_regions=['QLD1', 'NSW1', 'VIC1',

65 'SA1', 'TAS1'],

66 unit_info=unit_info)

67

68 volume_bids, price_bids = unit_inputs.get_processed_bids()

69 market.set_unit_volume_bids(volume_bids)

70 market.set_unit_price_bids(price_bids)

71

72 violation_cost = \

73 constraint_inputs.get_constraint_violation_prices()['unit_capacity']

74 unit_bid_limit = unit_inputs.get_unit_bid_availability()

75 market.set_unit_bid_capacity_constraints(unit_bid_limit, violation_cost)

76

77 unit_uigf_limit = unit_inputs.get_unit_uigf_limits()

78 market.set_unconstrained_intermittent_generation_forecast_constraint(

79 unit_uigf_limit, violation_cost)

80

81 ramp_rates = unit_inputs.get_bid_ramp_rates()

82

83 # This is the part that makes it time sequential.

84 if unit_dispatch is None:

85 # For the first dispatch interval we use historical values

86 # as initial conditions.

87 historical_dispatch = unit_inputs.get_initial_unit_output()

88 ramp_rates = time_sequential.create_seed_ramp_rate_parameters(

89 historical_dispatch, ramp_rates)

90 else:

91 # For subsequent dispatch intervals we use the output levels

92 # determined by the last dispatch as the new initial conditions

93 ramp_rates = time_sequential.construct_ramp_rate_parameters(

94 unit_dispatch, ramp_rates)

95

96 market.set_unit_ramp_rate_constraints(ramp_rates, violation_cost)

97

98 regional_demand = demand_inputs.get_operational_demand()

99 market.set_demand_constraints(regional_demand)

100

101 interconnectors_definitions = \

102 interconnector_inputs.get_interconnector_definitions()

103 loss_functions, interpolation_break_points = \

104 interconnector_inputs.get_interconnector_loss_model()

105 market.set_interconnectors(interconnectors_definitions)

106 market.set_interconnector_losses(loss_functions,

107 interpolation_break_points)

108 market.dispatch()

109

110 # Save prices from this interval

111 prices = market.get_energy_prices()

112 prices['time'] = interval

113 outputs.append(prices.loc[:, ['time', 'region', 'price']])

114

115 unit_dispatch = market.get_unit_dispatch()

116

117print("Run time per interval {}".format((time()-t0)/len(dispatch_intervals)))

118con.close()

119print(pd.concat(outputs))

120# time region price

121# 0 2019/01/01 12:00:00 NSW1 91.857666

122# 1 2019/01/01 12:00:00 QLD1 76.716642

123# 2 2019/01/01 12:00:00 SA1 85.126914

124# 3 2019/01/01 12:00:00 TAS1 86.173481

125# 4 2019/01/01 12:00:00 VIC1 83.250703

126# 0 2019/01/01 12:05:00 NSW1 88.357224

127# 1 2019/01/01 12:05:00 QLD1 72.255334

128# 2 2019/01/01 12:05:00 SA1 82.417720

129# 3 2019/01/01 12:05:00 TAS1 83.451561

130# 4 2019/01/01 12:05:00 VIC1 80.621103

131# 0 2019/01/01 12:10:00 NSW1 91.857666

132# 1 2019/01/01 12:10:00 QLD1 75.665675

133# 2 2019/01/01 12:10:00 SA1 85.680310

134# 3 2019/01/01 12:10:00 TAS1 86.715499

135# 4 2019/01/01 12:10:00 VIC1 83.774337

136# 0 2019/01/01 12:15:00 NSW1 88.113012

137# 1 2019/01/01 12:15:00 QLD1 71.559977

138# 2 2019/01/01 12:15:00 SA1 82.165045

139# 3 2019/01/01 12:15:00 TAS1 83.451561

140# 4 2019/01/01 12:15:00 VIC1 80.411187

141# 0 2019/01/01 12:20:00 NSW1 91.864122

142# 1 2019/01/01 12:20:00 QLD1 75.052319

143# 2 2019/01/01 12:20:00 SA1 85.722028

144# 3 2019/01/01 12:20:00 TAS1 86.576848

145# 4 2019/01/01 12:20:00 VIC1 83.859306

146# 0 2019/01/01 12:25:00 NSW1 91.864122

147# 1 2019/01/01 12:25:00 QLD1 75.696247

148# 2 2019/01/01 12:25:00 SA1 85.746024

149# 3 2019/01/01 12:25:00 TAS1 86.613642

150# 4 2019/01/01 12:25:00 VIC1 83.894945

151# 0 2019/01/01 12:30:00 NSW1 91.870167

152# 1 2019/01/01 12:30:00 QLD1 75.188735

153# 2 2019/01/01 12:30:00 SA1 85.694071

154# 3 2019/01/01 12:30:00 TAS1 86.560602

155# 4 2019/01/01 12:30:00 VIC1 83.843570

10. Nempy performance on older data (Jan 2013, without Basslink switch run)

This example demonstrates using Nempy to recreate historical dispatch intervals by implementing an energy market using all the features of the Nempy market model, with inputs sourced from historical data published by AEMO. A set of 100 random dispatch intervals from January 2015 are dispatched and compared to historical results to see how well Nempy performs for replicating older versions of the NEM’s dispatch procedure. Comparison is against ROP, the region price prior to any post dispatch adjustments, scaling, capping etc.

Summary of results:

Warning

Warning this script downloads approximately 54 GB of data from AEMO. The download_inputs flag can be set to false to stop the script re-downloading data for subsequent runs.

1# Notice:

2# - This script downloads large volumes of historical market data (~54 GB) from AEMO's nemweb

3# portal. You can also reduce the data usage by restricting the time window given to the

4# xml_cache_manager and in the get_test_intervals function. The boolean on line 22 can

5# also be changed to prevent this happening repeatedly once the data has been downloaded.

6

7import sqlite3

8from datetime import datetime, timedelta

9import random

10import pandas as pd

11from nempy import markets

12from nempy.historical_inputs import loaders, mms_db, \

13 xml_cache, units, demand, interconnectors, constraints

14

15con = sqlite3.connect('D:/nempy_2013/historical_mms.db')

16mms_db_manager = mms_db.DBManager(connection=con)

17

18xml_cache_manager = xml_cache.XMLCacheManager('D:/nempy_2013/xml_cache')

19

20# The second time this example is run on a machine this flag can

21# be set to false to save downloading the data again.

22download_inputs = True

23

24if download_inputs:

25 # This requires approximately 4 GB of storage.

26 mms_db_manager.populate(start_year=2013, start_month=1,

27 end_year=2013, end_month=1)

28

29 # This requires approximately 50 GB of storage.

30 xml_cache_manager.populate_by_day(start_year=2013, start_month=1, start_day=1,

31 end_year=2013, end_month=2, end_day=1)

32

33raw_inputs_loader = loaders.RawInputsLoader(

34 nemde_xml_cache_manager=xml_cache_manager,

35 market_management_system_database=mms_db_manager)

36

37

38# A list of intervals we want to recreate historical dispatch for.

39def get_test_intervals(number=100):

40 start_time = datetime(year=2013, month=1, day=1, hour=0, minute=0)

41 end_time = datetime(year=2013, month=1, day=31, hour=0, minute=0)

42 difference = end_time - start_time

43 difference_in_5_min_intervals = difference.days * 12 * 24

44 random.seed(1)

45 intervals = random.sample(range(1, difference_in_5_min_intervals), number)

46 times = [start_time + timedelta(minutes=5 * i) for i in intervals]

47 times_formatted = [t.isoformat().replace('T', ' ').replace('-', '/') for t in times]

48 return times_formatted

49

50

51# List for saving outputs to.

52outputs = []

53c = 0

54# Create and dispatch the spot market for each dispatch interval.

55for interval in get_test_intervals(number=100):

56

57 c += 1

58 print(str(c) + ' ' + str(interval))

59 raw_inputs_loader.set_interval(interval)

60 unit_inputs = units.UnitData(raw_inputs_loader)

61 interconnector_inputs = interconnectors.InterconnectorData(raw_inputs_loader)

62 constraint_inputs = constraints.ConstraintData(raw_inputs_loader)

63 demand_inputs = demand.DemandData(raw_inputs_loader)

64

65 unit_info = unit_inputs.get_unit_info()

66 market = markets.SpotMarket(market_regions=['QLD1', 'NSW1', 'VIC1',

67 'SA1', 'TAS1'],

68 unit_info=unit_info)

69

70 # Set bids

71 volume_bids, price_bids = unit_inputs.get_processed_bids()

72 market.set_unit_volume_bids(volume_bids)

73 market.set_unit_price_bids(price_bids)

74

75 # Set bid in capacity limits

76 unit_bid_limit = unit_inputs.get_unit_bid_availability()

77 cost = constraint_inputs.get_constraint_violation_prices()['unit_capacity']

78 market.set_unit_bid_capacity_constraints(unit_bid_limit, violation_cost=cost)

79

80 # Set limits provided by the unconstrained intermittent generation

81 # forecasts. Primarily for wind and solar.

82 unit_uigf_limit = unit_inputs.get_unit_uigf_limits()

83 cost = constraint_inputs.get_constraint_violation_prices()['uigf']

84 market.set_unconstrained_intermittent_generation_forecast_constraint(

85 unit_uigf_limit, violation_cost=cost

86 )

87

88 # Set unit ramp rates.

89 ramp_rates = unit_inputs.get_bid_ramp_rates()

90 scada_ramp_rates = unit_inputs.get_scada_ramp_rates()

91 fast_start_profiles = unit_inputs.get_fast_start_profiles_for_dispatch()

92 cost = constraint_inputs.get_constraint_violation_prices()['ramp_rate']

93 market.set_unit_ramp_rate_constraints(

94 ramp_rates, scada_ramp_rates, fast_start_profiles,

95 run_type="fast_start_first_run", violation_cost=cost

96 )

97

98 # Set unit FCAS trapezium constraints.

99 unit_inputs.add_fcas_trapezium_constraints()

100 cost = constraint_inputs.get_constraint_violation_prices()['fcas_max_avail']

101 fcas_availability = unit_inputs.get_fcas_max_availability()

102 market.set_fcas_max_availability(fcas_availability, violation_cost=cost)

103 cost = constraint_inputs.get_constraint_violation_prices()['fcas_profile']

104 regulation_trapeziums = unit_inputs.get_fcas_regulation_trapeziums()

105 market.set_energy_and_regulation_capacity_constraints(regulation_trapeziums,

106 violation_cost=cost)

107 scada_ramp_rates = unit_inputs.get_scada_ramp_rates(inlude_initial_output=True)

108 market.set_joint_ramping_constraints_reg(

109 scada_ramp_rates, fast_start_profiles, run_type="fast_start_first_run",

110 violation_cost=cost

111 )

112 contingency_trapeziums = unit_inputs.get_contingency_services()

113 market.set_joint_capacity_constraints(contingency_trapeziums, violation_cost=cost)

114

115 # Set interconnector definitions, limits and loss models.

116 interconnectors_definitions = \

117 interconnector_inputs.get_interconnector_definitions()

118 loss_functions, interpolation_break_points = \

119 interconnector_inputs.get_interconnector_loss_model()

120 market.set_interconnectors(interconnectors_definitions)

121 market.set_interconnector_losses(loss_functions,

122 interpolation_break_points)

123

124 # Add generic constraints and FCAS market constraints.

125 fcas_requirements = constraint_inputs.get_fcas_requirements()

126 cost = constraint_inputs.get_violation_costs()

127 market.set_fcas_requirements_constraints(fcas_requirements, violation_cost=cost)

128 generic_rhs = constraint_inputs.get_rhs_and_type_excluding_regional_fcas_constraints()

129 market.set_generic_constraints(generic_rhs, violation_cost=cost)

130 unit_generic_lhs = constraint_inputs.get_unit_lhs()

131 market.link_units_to_generic_constraints(unit_generic_lhs)

132 interconnector_generic_lhs = constraint_inputs.get_interconnector_lhs()